- 12 Sep, 2023

September 2023 Mortgage Rate Swing: Is It Time to Jump In?

Insights of 2023 - When will mortgage rates go down?

Planning to purchase a home? You might have come across the term mortgage rates. They are one of the most commonly used terms and play a significant role in your mortgage application journey.

Whether you are looking to get a new mortgage, planning to refinance, or avail reverse mortgage, the mortgage rates play a crucial role in determining your application status. The world of real estate and finance is a dynamic landscape where the situations don’t remain the same. It keeps changing as the economy expands and new buildings are being constructed.

“Every person who invests in well-selected real estate in a growing section of a prosperous community adopts the surest and safest method of becoming independent, for real estate is the basis of wealth.”

- Theodore Roosevelt, the former U.S. President

As we venture into September, it is essential to start your research by examining the mortgage rates as it is buzzing with anticipation and speculation from prospective and existing home buyers.

We know what you’re thinking! When will mortgage rates go down? We will answer your question by understanding the existing mortgage scenes in the United States, and past mortgage trends, and finally see what mortgage rates in 2024 will be like.

By the end of this blog, you should be able to decide whether now is the right time to jump into a mortgage application process.

Let’s get into the details!

The current mortgage scenario - What’s it like?

Before finding the answer to this question, we must first understand the current situation. With the rise in mortgage rates in more than two decades, September could be a light of hope, but don’t expect the rates to come down drastically.

There have been some fluctuations in September, and these ups and downs are primarily due to economic factors and market dynamics. Bond prices highly influence mortgage rates. Technically, when bond prices go up the mortgage interest rates come down. This usually happens as lenders link their interest rates to treasury bond rates.

The Federal Reserve’s decisions regarding monetary policy also play a significant role. If the Fed raises or lowers the interest rates, it directly impacts short-term interest rates and indirectly affects long-term mortgage rates.

In the past few months, there has been speculation about the potential rise in interest rates by the Federal Reserve to deal with the rising inflation. Due to this, most individuals worry that their mortgage rates will increase. However, it is important to note that mortgage rates are noticeably higher to start the new week of September as some lenders increased their costs nearly on Friday.

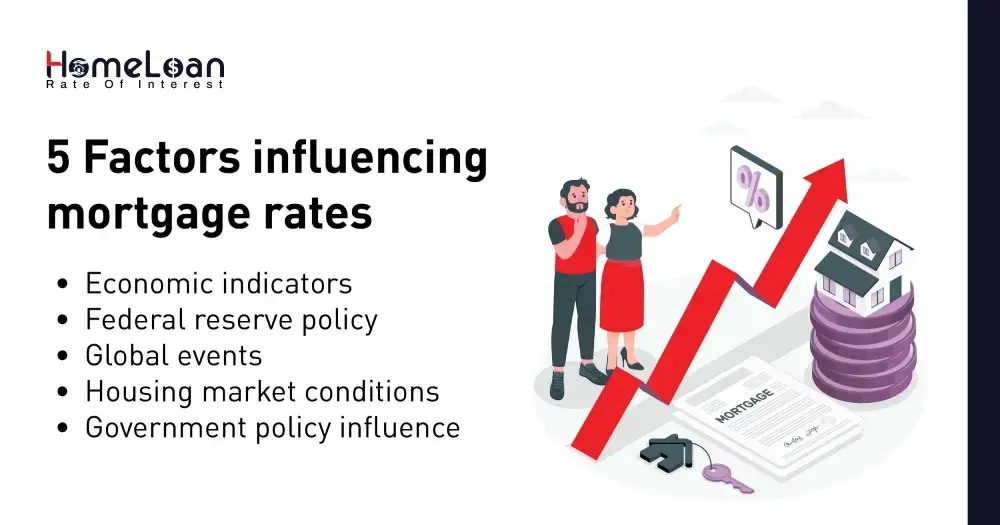

5 common factors that influence mortgage rates

If you’re purchasing your home, be it for the first time or using it to tap into accumulated equity, it is important to understand what goes behind these mortgage rates. You need to know the factors that are used to determine the mortgage rates. Let’s see what these factors are:

-

Economic indicators

The increase and decrease in mortgage rates are highly influenced by economic indicators such as GDP growth, employment rates, and inflation. If the economy is performing well and strong, the mortgage rates might be higher as central banks may raise interest rates to control inflation.

-

Federal Reserve policy

As discussed above, the Federal Reserve’s decision on interest rates directly impacts short-term borrowing costs. Their actions and moves can have a ripple effect on the entire financial market, affecting long-term mortgage rates.

-

Global events

Unexpected changes in the global economy can also impact mortgage rates. This can drive investors to seek the safety of U.S. Treasury bonds, influencing yields and, subsequently changing the mortgage rates.

-

Housing/Real estate market conditions

The demand for housing and people who are increasingly looking for houses can also impact the mortgage rates market. If there is a gap in the amount of houses being sold, due to less demand, there could be a decrease in mortgage rates.

-

Government policy influence

Government-sponsored enterprises like Fannie Mae and Freddie Mac also play a significant role in affecting the availability and cost of mortgage credit.

Time to examine the data!

Between the two business days (banks were closed on Monday), the average lender is up between 0.125% and 0.25% from Thursday afternoon.

US mortgage rates rose for a second straight week, reaching the highest since November.

The 30-year fixed-rate mortgage averaged 7.21 percent as of September 6, 2023, increased from last month when it averaged 6.96 percent. A year ago at this time, the 30-year FRM averaged 5.23 percent.

The 15-year fixed-rate mortgage averaged 6.58 percent, down from last week when it averaged 6.30 percent. A year ago at this time, the 15-year FRM averaged 4.38 percent.

Historical mortgage rate trends

To understand and predict where mortgage rates are headed in the future, we need to look back at past rates. Over the past few years, mortgage rates have experienced highs and lows very rarely.

To go back in time around the early 2020s, mortgage rates were historically low especially due to the impact of the Covid-19 pandemic. The Federal Reserve took rapid action in order to encourage economic activity.

However, as the Covid-19 pandemic started to settle down in late 2022 and early 2023, the mortgage rates gradually started increasing. Due to concerns of rising inflation, the Federal Reserve began to increase interest rates. Now that we are in September, mortgage rates are rising straight even during the second week.

Do mortgage rates follow a pattern?

By analysing historical mortgage rate trends, some patterns influence the rates such as:

-

Seasonal variations

Mortgage rates vary as per season, and as per the past variations, rates have been a bit lower during the fall and winter months compared to the summer and spring where the rates have been increased slightly. This is due to factors such as homebuyer’s likes and preferences and prevailing market conditions.

-

Economic cycles

Mortgage rates are affected by economic cycles. When there is an economic expansion, rates usually rise, and the Fed tries to control inflation. On the contrary, when there is a downfall, rates tend to fall too.

-

Federal Reserve impact

As discussed earlier, the Fed immediately impacts the mortgage rates due to changes in their monetary policies. If you are an avid follower of mortgage rates, watch out for the Fed’s news and you will know whenever the rates are likely to increase.

Mortgage rates 2024 - What lies ahead?

Now that we have seen the trends of mortgage rates in 2023, it is time for us to discuss the mortgage rates in 2024. While forecasts and predictions just give you insights into what might happen and make informed decisions, they cannot give you accurate information. Here are some key projections:

-

Many financial experts anticipate that mortgage rates might increase gradually as we progress into the year 2024. The prime reason is, Inflation! However, the pace at which these changes are going to take place is uncertain.

-

If the Federal Reserve opts to hike rates more cautiously, rates can be stable and benefit homebuyers and homeowners. In the end, it is important to address that the economic landscape in 2024 can be uncertain. Factors like global pandemic, geographical changes, and political changes can influence the rates to go down or rise.

Should you wait or act now?

Let’s accept reality! Mortgage rates will continue to rise or come down due to above-listed factors. We understand that the dilemma is real, whether you need to wait for a potential decrease in the mortgage rates or take action now depends on an individual’s urgency and financial situation.

4 easy-to-implement strategies to make better decisions

Whether you are willing to take action or wait, use these strategies to deal with mortgage rate fluctuations effectively:

-

Rate lock

If you’re comfortable with the current rates, you can consider a rate lock. This offers you convenience in protecting your rates even if there is an increase while you complete your mortgage process.

-

Refinancing

This can be an added advantage if you’re a current homeowner. With refinancing, you can secure a lower rate which can lead you to lower monthly payments and an opportunity to shorten your loan term.

-

Budget and credit

You can use the waiting period to review your budget and improve your credit score as a solid financial profile can help you secure better rates when you’re planning to buy or refinance.

-

Expert Guidance

You can choose to consult with mortgage professionals and financial experts. They are professionals to help you make the right decision and provide insights tailored to your situation.

The question of "When will mortgage rates go down?" still remains a concern for potential homebuyers due to prevailing market conditions and the Fed’s decisions. It is challenging to predict absolute rate fluctuations and hence it is advisable to stay informed about your economy’s trends.

As you consider your mortgage options, keep in mind that the decision to buy a home or refinance should align with your long-term financial goals. Whether you choose to take action or wait for the rate to decrease, it is essential to consult with a mortgage professional. HLRI can help you in finding the right financing options for your new or existing home based on your needs. We hope you lock in the best mortgage rate right away!